In case of high-value transactions, real estate companies, government entities, colleges or other large corporations/ institutions typically don’t accept general/ personal cheques from individuals or firms to receive payment because there is always a risk of dishonour of the cheque. Therefore, such organisations/ institutions instruct the individuals/ entities to enclose a bankers cheque or demand drafts in order to pay the amount.

In this article, we will discuss what exactly the banker cheques are? And how they are different from demand drafts. You will also be able to understand the following query by the end of this article.

- What is a Bankers Cheque?

- Features of bankers cheques

- Purpose of Bankers Cheque

- Bankers Cheque Charges

- Difference between bankers cheque and demand drafts

- Frequently Asked Questions (FAQ)

Table of Contents

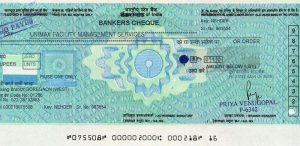

Banker’s Cheque:

A banker cheque, also known as Pay Order/ banker’s draft/ Teller’s cheque in the United States is nothing but a special cheque issued by the banks on the behalf of their customers or itself on a prepayment basis. Therefore, such cheques are never dishonoured as the payment of such cheques is already deposited in the banks.

Bankers cheques are issued in the favour of specific persons/ entities against advance payment to whom the applicant is required to pay a certain amount. The validity of bankers cheque is 3 months from the date of issue and can be further re-validated if expired.

The banker’s cheques are considered the most secured types of cheques as compared to others as it is guaranteed by the banks itself. It is a non-negotiable instrument that can’t be transferred to anyone at any circumstances. Moreover, a bankers cheque can neither be stopped nor be cancelled at any conditions.

You must have been asked to attach a bankers cheque or demand draft whenever you had been taken admission in the college or as security (token money) at the time of application of government/ private tenders or during the purchase of new property/ apartment as booking amount.

Purpose of issuing Bankers Cheque

There are primarily two scenarios wherein the banker’s cheques are issued. The first one is on the behalf of applicants/ bank’s customers, however, the second one is for the clearance of the bank’s own expenses/ dues. Some other significant circumstances are as follows where the bankers can be issued.

- Payment of maturity amount in case of fixed deposits

- Payment of balance amount on the permanent closure of deposit (saving/ current/ OD/ RD) accounts

- Rent Payment for building/ spaces

- Electricity/ water bill payments

- Payment of service charges of third party service providers/ agencies

- Other official and maintenance expenses

In addition, when the banker’s cheque is issued on customer behalf.

- For payment of college/ institutions fees

- As a booking amount during the purchase of apartments/ plots

- As a security deposit during government/ corporations tenders

- For security deposit in auctions

- Other high-value payments

Features of Bankers Cheque:

- All bankers cheques are preprinted and non-negotiable.

- Banker cheque can’t be dishonoured

- It can be revalidated if expired and duplicate banker cheque can be issued if lost for nominal fees.

- Bankers cheques are accepted locally.

- No risk of default from both drawer and payee perspectives

Bankers Cheque Charges:

The banker’s cheques can be obtained for nominal fees charged by the banks based on amounts.

- For the value up to Rs 5,000/- (Rs 25/-)

- For value Rs 5,000/- to 10,000/- (Rs 50/-)

- For value Rs 10,000/- to 1 lac (Rs 6 per 1000/- and a min of 60/-)

- For value above Rs 1 lac ( Rs 4/- per thousand and a min. of Rs 600/- and Max Rs 2,000/-)

Note:

- All the above charges are inclusive of Goods and services taxes (GST)

- No cash handling charges will be levied for the issuance of bankers cheque in addition to above charges in case of cash transactions.

- Courier charges Rs 150/- + GST will be applicable for delivery of bankers cheque in case of online request for issuance of banker cheque.

In addition, the issuance of duplicate banker cheque and revalidation a fee of Rs. 200/- + GST shall be applicable.

Difference & Similarities between Bankers Cheque and Demand Drafts:

Although both bankers cheques and demand drafts (DD) are drawn against advance payment and hence ensure the guarantee of payments, yet there are two major differences is that the baker’s cheques are payable locally, on the other hand, demand drafts are payable at different cities.

- The banker’s cheque is payable at any branch of the same bank within the city, on the other hand, demand drafts are payable at any branch of any city.

- The second major difference between banker cheque and demand drafts (DD) is that a banker cheque can be issued by the banks on the behalf of their customers (individuals or business entities) or banks itself for self-use, on the other hand, a demand draft is issued by the banks but on the behalf of their customers or individuals or firms only.

However, there are some similarities between bankers cheques and demand drafts which are:

- Both are non-negotiable instruments that cannot be transferred to any person/ entities.

- Both are issued by the banks on behalf of their customers or non-customers.

- Both are issued against advance payment

- Hence both cannot be dishonoured

- The validity of both the instruments is 3 months from the date of issue.

Conclusion:

In a nutshell, we can conclude that the banker’s cheques and demand drafts facilitate high-value transactions to minimize the risk of defaults from buyers/ drawers ends. It is generally preferred when the payee wants 100% payment guarantee from the buyers/ clients because a bank itself guarantees the settlement of payment in future. This is because a banker cheque can be obtained only against advance payment.

Hope this article will clear all your queries regarding bankers cheques, their uses, features and fees.

Related Articles:

How to lodge a complaint in the Banking Ombudsman?

Major functions of commercial banks

References: 1) sbi.co.in (source) 2) Wikipedia

Frequently Asked Questions (FAQ):

Q.1 Can a Bankers Cheque be cancelled?

Ans: No, The banker’s cheques cannot be cancelled because the bank itself is responsible to pay the mentioned amount to the beneficiary.

Q.2 Can a banker’s cheque be obtained against a cash deposit?

Ans: Yes, one can request the banks to draw a bankers cheque against cash without any extra charge.

Q.3 Can a banker’s Cheque be fake?

Ans: A bankers cheque has some security features like security thread, colour-shifting ink, watermarks as well as a bond paper which makes it more secure.

Q.4 Is a bankers cheque as good as cash?

Ans: No, because when it comes to high-value transactions, cash transactions are typically not safe as there is no documented proof of happened transaction, on the other hand, in case of bankers cheque, you have evidence of the transaction, hence you can file a sue in case of any default.

Q.5 What is the validity of a banker cheque?

Ans: 3 (three) months from the date issue

Q.6 What if the banker’s cheque is expired?

Ans: If the banker’s cheque is expired, it can be re-validated against a nominal fee to the banks.

Q.7 What if the banker’s cheque is lost or damaged?

Ans: If the banker’s cheque is lost or damaged, the drawer can request the bank to issue a duplicate bankers cheque against some fee.

If a customer requests for issuing a bank draft, can he be issued bankers cheque in place of bank draft

Thanks, Sohan for your query.

Yes, He can be issued a bankers cheque instead of a DD.