Bank deposits simply refer to placing your money into banks or financial institutions for convenience, saving and safeguarding your money from theft and other risks of losses. To deposit your funds in a bank, you need to open a bank account in any commercial or other types of bank.

Also, the bank provides some interest against your balance amount at a certain rate called an interest rate. The interest rate varies from bank to bank and time to time and also depends upon the types of bank accounts you hold.

There are several other benefits of opening a bank account such as ATM service, Loan facility, Credit card, money transfer, receiving instant payment from anywhere etc.

Accepting deposits and allocation of credits ie. granting loans/advances are the major functions of commercial banks. Commercial banks play a significant role in the Indian financial system. Any Individual or business enterprise or social entities can entertain the services of commercial banks or other financial institutions by opening a bank account in the respective banks.

In this topic, we will discuss various types of bank deposits or accounts in India.

Table of Contents

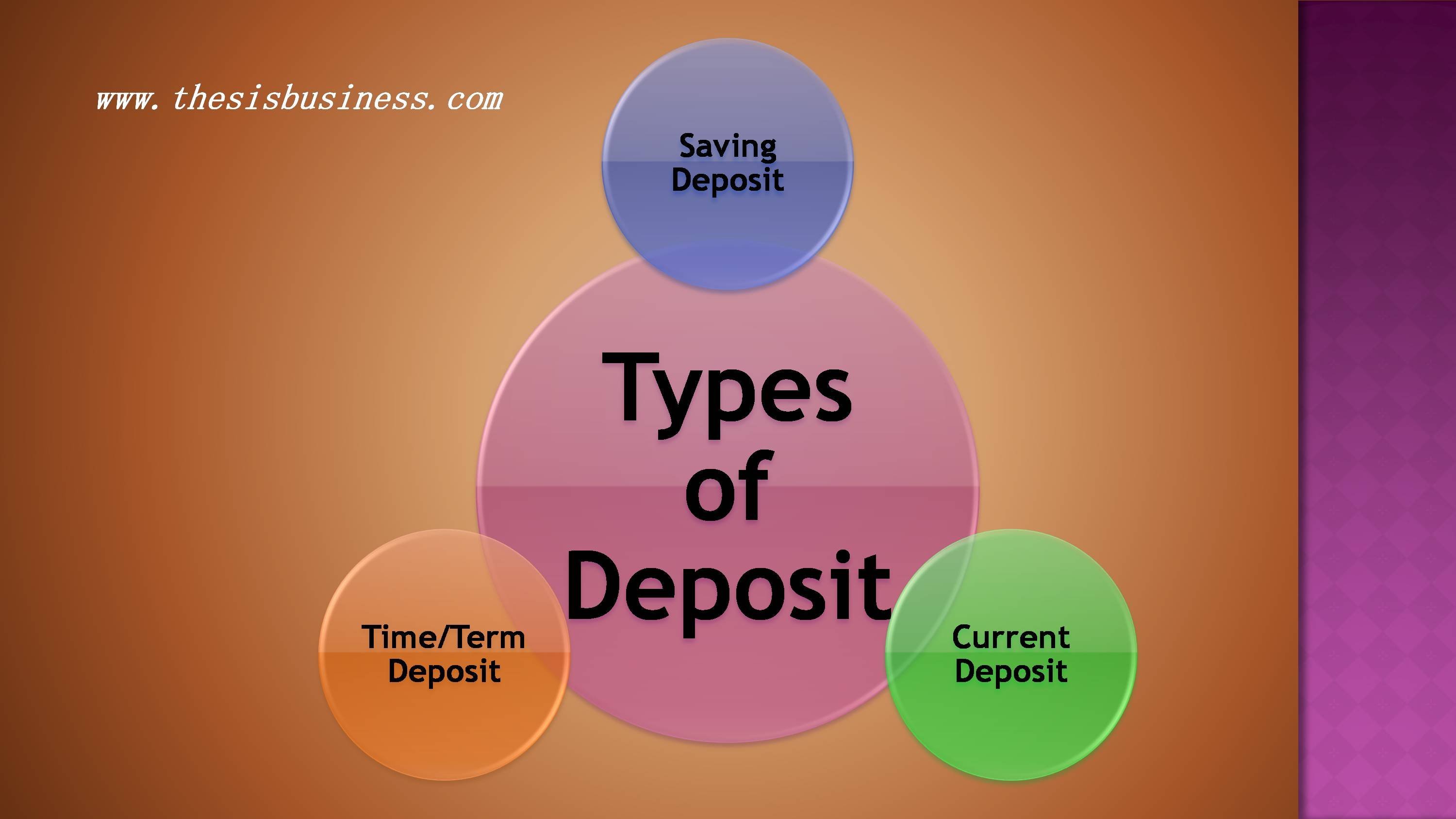

Types of Deposit:

There are basically three types of deposits in India which we are going to explain one by one in details.

- Saving Deposits

- Current Deposits

- Time/ Term Deposits

1) Saving Deposits:

Saving Deposits are those bank deposits which has to be paid on demand, this means whenever the depositor demands his money, the bank has to pay his money back, however, there is a norm of maintaining minimum balance amount in his bank account.

The depositor can withdraw his amount either by cheque or by withdrawal slip or using ATM from his respective branch. In these days, account holders can also withdraw their money through AEPS (Aadhar Enabled Payment System).

A Saving Accounts can be operated by either

- Self

- Authorised Signatory

- Minor Accounts are operated by the guardian

A saving account can be opened with or without cheque book and also nomination facility is available for these accounts.

Who is eligible to open a Saving Account?

Any person who are the citizens of India whether they are Resident or Nonresident eligible to open a saving account in any bank. In addition, societies, trust, associations, clubs or minors along with (operated by) their guardian can also open a saving account in India.

2) Current Deposits:

Current Deposit is also a demand deposit which means the banker is bound to pay the money if the customer demands. This is a running account and the operator has rights to deposit or withdraw anytime subject to fulfil minimum balance criteria. These accounts have the facility of withdrawal by cheques or a simple letter or by ATM Card (Debit Card).

No interest is payable on current accounts credit balance instead on debit balance, interest is charged to the account on a monthly basis. Also, the debit interest is charged based on daily debit products.

There is no restriction on the number of transactions in the current account, however, service charge is levied based on the number of transactions and average credit balance in the account.

Current account can be operated either by self or survivor or by authorised signatory.

Temporary Overdraft may be permissible for a current account upon a written request by the account holder.

Who is Eligible?

A current account can be opened by:

- Individuals

- Private or Public Limited Companies

- Proprietorships or Partnership Firms

- Societies, Associations, Trust or Clubs

3) Time/ Term Deposits:

Time deposits or term deposits are some kinds of agreement between depositor/ customer and bank specifying the amount of deposit, time period of deposit and returns (rate of interest) on deposits. In case of time/ term deposits, a fixed amount of funds is deposited in the bank by the customer for a stipulated time period at a specified rate of interest.

There are 4 different schemes under term deposits.

- Fixed Deposit (Monthly, Quarterly, half-yearly, Annually)

- Cumulative (Reinvestment) Plan Deposit

- Recurring Deposit

- Flexi-Term Deposit

a) Fixed Deposit and Cumulative Plan Deposit:

In a fixed deposit, the customer deposits a lump sum amount of money in his bank account for a predefined time period and the bank promises a fixed rate of interest to the customer. The tenure may be ranging from 7 days to 10 years and interest rate offered by the bank is higher than demand (saving bank) deposits and computed as simple interest or compound interest on quarterly, half-yearly or annual basis.

The interest rate may vary from 5.5% to 7% depends upon banks (Public or private) and market interest rates (MIBOR). The senior citizens (above 60 years) entitle for an additional 0.5% of the interest rate.

A Tax Deduction at Source (TDS) is deducted on interest income (interest earned) at the time of maturity, however, an interest income below Rs 40,000/- is exempted from tax.

Premature Closer or Foreclosure refers to the withdrawal of money before maturity period and in case of such withdrawal, the interest rate is calculated 1% less applicable for the reduced period.

The customer has the following options on maturity.

- Renew the deposit – Either principal amount and interest or principal only

- Partial Renewal

- Renew with an additional amount

If the customer doesn’t approach the bank immediately on the maturity of the deposit, the bank will transfer the entire amount along with interest to a separate account called Unclaimed or Overdue Deposit.

The customer can avail a loan of 70 to 90% of the total amount against the fixed deposits and the interest may be charged over 2% of term deposit interest rate. Moreover, term deposit can’t be withdrawn till the repayment of the loan.

b) Recurring Deposit:

Recurring deposit facilitates to save a certain proportion of one’s income regularly on a monthly basis. Recurring deposits are those term deposits in which a certain amount of money is deposited on a monthly basis and also the rate of interest is the same as fixed deposits.

Unlike fixed deposits, there is no need to deposit a fixed or lump sum amount at once and also no TDS (Tax Deduction at source) is applicable to interest income at the time of withdrawal. You need to deposit a minimum amount like an instalment which could be Rs 100/- every month. You can also request the bank to deduct that amount automatically on the due date.

You can also avail the benefit of loan up to 70 to 90% against the amount deposited in the recurring deposit account. However, like fixed deposits, premature withdrawal is not permissible but one can close the account before maturity date by paying a penalty.

c) Flexi Deposit:

Flexi deposit is basically the combination of both time and demand deposit. In the case of Flexi deposits, the customer not only entertains the interest rate of the term deposit but also the flexibility of demand deposit.

Although different banks use different terminology for these types of deposit yet some commonly used names are Quantum Optima, Sweep Account Deposit.

Generally, the bank declares a minimum opening balance (for example 25,000/-) for the opening of such accounts and some proportion of this amount ( say 20,000/-) will be deposited as time deposit in predefined multiple (say multiple of 1000) and rest of the amount is placed as a demand deposit and also the customer has the flexibility to choose the terms of deposit.

Conclusion:

Hope you have understood some of the major types of bank deposit in India. In a nutshell, there are mainly three types of deposit viz Saving deposit, current deposit and term deposit. We can simply understand, in saving deposit there is a limitation of the number of transactions whereas in current deposit, no restriction on the number of transactions, however, in case of term deposit, as the name suggests, there are certain term and conditions between depositor and bank which will be followed by both the parties.

Recommended Article:

Difference between commercial banks and cooperative banks

Difference between Commercial bank and Central bank

References: Bank of Baroda